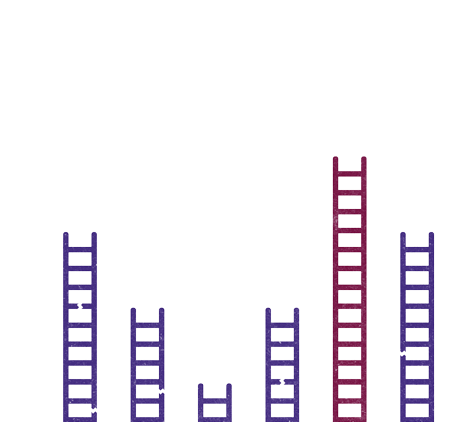

Appetite for investment grows among mid-market leaders

International business

Mid-market business leaders plan to increase investment over the next 12 months, specifically in technology, research and development and staff.